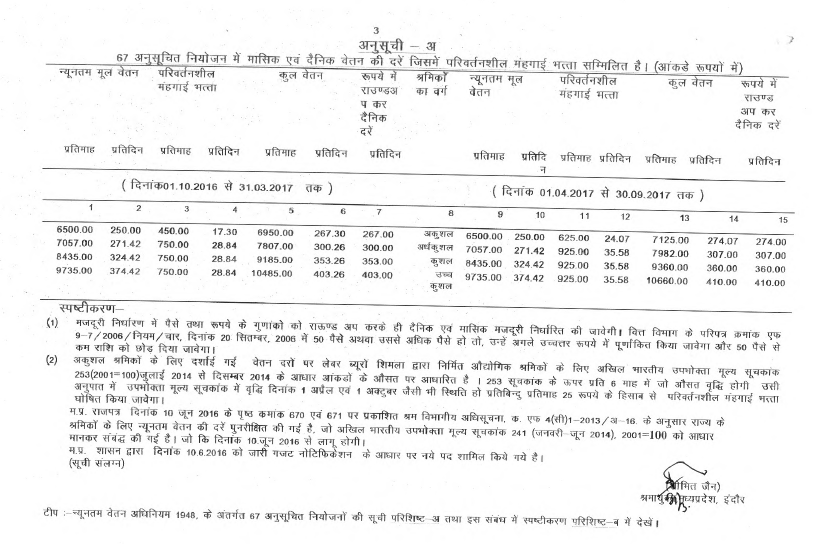

On 1st May 2017, EPFO announced the launch of the facility to withdraw EPF and EPS online. Let us see the procedure and conditions of online EPF withdrawal facility in detail

As of now, it is a tedious task to apply for withdrawal. The process involved physical application to move from one authority to another authority. Usually, this whole process used to take around 30 days of time.

However, EPFO since long planning to do this facility. Now EPFO released the press note on the same.

You can complete the whole process online and you neither needs to interact with the employer and nor with EPFO field office to submit the online claim. The claim submitted by the you would flow in soft form to EPFO database where it will be processed and the member’s bank account credited.

You are not required to give any supporting document while preferring online EPF Part Withdrawal case. If you are applying online will be taken as his self-declaration for preferring the advance claim.

Who can withdraw EPF and EPS online?

There are certain conditions for utilizing this facility to withdraw EPF and EPS online. They are as below.

# You must have activated UAN Card.

# You must be linked Aadhaar with EPF.

# You must be using the same mobile number which is linked with your Aadhaar. Because EPFO will send you OTP (One Time Password) for authenticating the claim process online.

# Your bank account along with IFSC code should be linked in EPFO database.

# Permanent Account Number (PAN) should also be linked in EPFO database for EPF Final settlement claims in case his/her service is less than 5 years.

If these two conditions are satisfied, then you can withdraw EPF and EPS online.

What types of EPF claims can be withdrawn online?

# You can withdraw your EPF amount online.

# You can withdraw your EPS (Employee’s Pension Scheme) amount online.

# You can use this online platform for partial or advance withdrawal of EPF .

How to withdraw EPF and EPS online?

Below are the steps involved of how to withdraw EPF and EPS online.

As of now, the information is limited. Hence, I will be sharing the information which is available at this time. I will update the same, once it is live on EPFO portal.

1. Login to UAN portal.

2. Check that KYC and service shown against your UAN are correct.

3. Select which option of withdrawal you want to select like EPF Withdrawal, EPS Withdrawal or Partial or Advance EPF withdrawal.

Once you submit the request, then for authentication purpose, OTP will be sent to your Aadhaar based registered mobile number.

1.Authenticate the same by entering OTP.

2. Then submit for withdrawal.

The process of withdraw EPF and EPS online is now available and the process is explained as below

Step 1-Login to EPFO Unified Portal for Members

Step 2–

Then on the homepage of Unified Portal, select the option “Online Services” tab. Here, you can withdraw EPF and EPS online and also can check the claim status online

Also enclosed is the FAQ & detail Process flow

👉Faq on Online Claim

ONLINE CLAIM CHECK ELIGIBILITY AND SUBMISSION FLOW DIAGRAM

👉Eligibility Check